Today's links have a range of pieces discussing China's development model and its possible slowdown. In the Reuters' piece, a range of analysts describe the middle-income trap awaiting China. That is the historical phenomenon of developing economy growth stagnating once average incomes hit the $7000 range. Here's the money quote from the piece:

According to data compiled by the late economic historian Angus Maddison and cited by Morgan Stanley, about 40 economies have attained a per capita GDP level of $7,000 over the past century or so.

Remarkably, the average growth rate of 31 of those 40 countries was 2.8 percentage points less in the decade after the $7,000 inflection point was reached than in the preceding decade.

Japan and South Korea hit the $7,000 mark around 1969 and 1988, whereupon their annual average GDP growth rates decelerated in the following decade by 4.1 and 2.4 percentage points respectively, Morgan Stanley calculates.

China's per capita GDP today is less than $4,000 at market exchange rates, but the bank reckons it reached Maddison's magic number, which is based on purchasing power, in 2008.

"If history is a guide and the law of gravity applies to China, China's economic growth is set to slow," Morgan Stanley said in a recent report.

China's slowdown might be gentler given its continental-sized economy and the potential for catch-up in the poorer interior. But the development experience of its neighbors, including Taiwan, is a benchmark too powerful to ignore.

Morgan Stanley has penciled in average GDP growth of 8.0 percent a year from 2010-2020, down from 10.3 percent from 2000-2009.

Slower, though, can mean a better balance. In Japan and South Korea consumption and labor income rose sharply as a share of GDP in the decade after growth peaked, while their service sectors expanded strongly.

There is a double blow here for Australia. Not only is it a slower China, but its growth mix is less favourable to the key commodities of iron ore and metallurgic coal as it moves away from fixed investment and towards consumption.

This blogger agrees this is a likely outcome for three reasons. First, China is experiencing a shift to higher labour costs. Second, external pressures arising from the trade imbalance with the US give it no choice but to rebalance internally. And third, this blogger sees no evidence that China will be able to make the political shift to greater freedoms needed if it is to further liberalise its economy and escape the trap like Korea has been able to. As a continental economy, however, China should fare better than Japan because of its greater growth sources.

Now, the course of development never did run smooth, and this blogger does not expect this change in Chinese growth to happen overnight. Indeed, as Michael Pettis argues when comparing internal rebalancings for Japan and China today:

It seems to me that the longer the Japanese distortions (especially repressed interest rates) were in place, the more debt built up, the more the large and growing capital-intensive sector required cheap capital to survive, and the harder it was to adjust interest rates. China seems to me very reliant on the same set of polices, especially very cheap capital, and it may be just as hard for them to adjust. For those who haven’t read my earlier pieces and wonder what cheap capital has to do with domestic imbalances, remember that cheap capital transfers income from net savers (households) and so reduces household consumption. It is, in my opinion, the single most important cause of China’s low consumption.

To get back to Japan’s experience, remember also that when the yen was finally forced to revalue after 1985, as the renminbi will almost certainly be, Tokyo responded to the potential slowdown with the only tool it had – investment expansion and lower real rates. This is also the only tool Beijing has, and it will almost certainly use it, making the current account adjustment even worse.

In that event, then, China's slowdown is actually likely to be preceded by a blowoff period in its fixed-investment. Even though Chinese authorities are well aware that this is a danger.

So, we have two possible scenarios for a slowing China. The first is a slow stagnation as rising costs and exchange rates crimp competitiveness or a response to that of ramping up credit and blowing off.

This blogger has no idea which of these is going to happen. And to a degree it doesn't matter.

The bottom line is that it will, most likely, happen. Where does that leave Australia?

The first point we need to understand is that commodity markets are now operating like asset markets, as discussed in this post. That is, they're driven as much by liquidity and behaviour as they are the fundamentals of supply and demand.

Such markets do not rise and fall gently. They form bubbles, such as we have now in some metal prices, and then suddenly, some shock sends them through the floor. So, for a start, commodity prices are unlikely to signal changes in China by falling in advance of, or in the early stages of, any slowdown. They will more likely follow it all at once.

Afterwards, as the growth of the China bid diminishes or reaches a plateau in global commodity markets, then the knock-on effects for commodity prices will be very large. The below chart shows how the China bid has raised the price of Australian resource exports to all destinations. When China slows they will all fall.

When that happens this blogger expects the chart below to matter a great deal. Australian productivity growth is at its lowest in the history of the chart. Moreover, the currency is at record highs and the real exchange rate (including inflation) is higher still. In short, Australian competitiveness is galloping backwards.

Even more disturbingly, these chickens are coming home to roost first in our non-resource tradable sectors, meaning our external position is even more dependent upon resource exports.

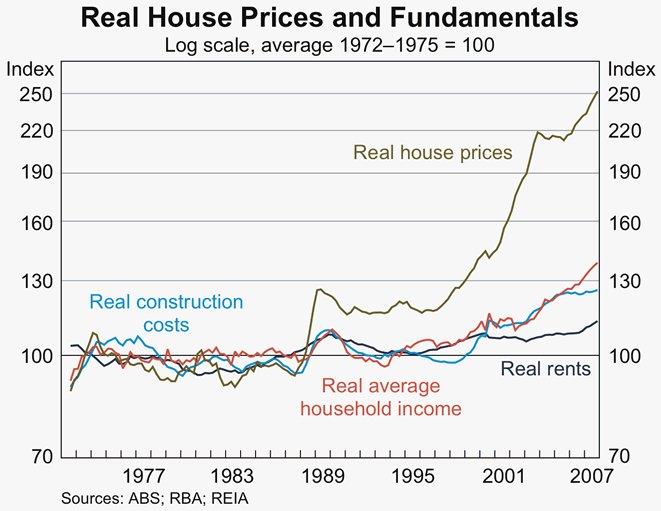

Why has this not mattered so far? It's pretty simple. Take a look at two lines on the below chart. The first and most obvious to note is house prices. Second, and just as importantly, is the rocketing red line "real average household income".

Australia's lack of competitiveness has been masked by wealth effects in housing and the extraordinary income flood from high commodity prices expressed through low unemployment, rising wages, high equity prices and lower taxes.

So, what happens when the commodity prices fall? If we're lucky, it will only be the slow reverse of these five factors as we get poorer.

If we're unlucky, and it happens all at once, this blogger's great fear, the world will run out of patience quickly and reprice our debt. Then the following chart is all that will matter:

BTW, this is behind the times. The blue line is now through the top of the chart.

4 comments:

Apologies to those who posted comments on this. I removed them by mistake...

You've broken all the links to it as well.

Any chance you could fix it so the original URL works? i.e.

http://housesandholes.blogspot.com/2010/10/slow-australia-not-for-faint-of-heart.html

Afraid I'm not that bright.

I have enjoyed reading your articles. It is well written. It looks like you spend a large amount of time and effort in writing the blog. I am appreciating your effort. .

Houses in Australia

Post a Comment