US economy growing at 2%, below pre-recession level. Calculated Risk

Still riding inventories. David Rosenberg

Consumers still in funk. PMI not. Zero Hedge I, II

ForeclosureGate now hitting sales. Bloomberg

Why this US cycle is different. Econompic

China dependency index. The Economist

China overstretched, overvalued. FT

Clancy Yates is wrong on bank competition.

Terry McCrann thinks we don't get it about China. The Australian

India may ban ore exports. Bloomberg

2011 ore talks underway, demand soft. Reuters

And for those with too much time on their hands, find below a recent IMF report on the spillover effects of China on the world economy:

wp10165

Saturday, October 30, 2010

Friday, October 29, 2010

Royally, globally, screwed...

Australian dollar versus the US dollar:

And the Korean Won:

And the Thai Baht:

And the South African Rand:

And the Chilean Peso:

And the Brazilian Real:

And the British Pound:

And the Euro:

And the Korean Won:

And the Thai Baht:

And the South African Rand:

And the Chilean Peso:

And the Brazilian Real:

And the British Pound:

And the Euro:

Links October 29: Dollar shocker

IMF endorses this blog: dollar overvalued, need giant RSPT. The Age

China's growing costs. Gavyn Davies

ForclosureGate linkfest. Barry Ritholz

European schlerosis: FT, WSJ, Alphaville (h/t Naked Capitalism)

See also Delusional Economics

Bond bull death. Econompic, Calculated Risk

End of the Wen put. William Pesek

Mr Smith goes to Canberra. Peter Martin

Eeeuuuw. And for a more sickening take. Matthew Stevens

Vale's big African bet. Mining Weekly

China's growing costs. Gavyn Davies

ForclosureGate linkfest. Barry Ritholz

European schlerosis: FT, WSJ, Alphaville (h/t Naked Capitalism)

See also Delusional Economics

Bond bull death. Econompic, Calculated Risk

End of the Wen put. William Pesek

Mr Smith goes to Canberra. Peter Martin

Eeeuuuw. And for a more sickening take. Matthew Stevens

Vale's big African bet. Mining Weekly

Thursday, October 28, 2010

Westpac drops a clanger (updated)

This blogger will analyse at greater depth the new Westpac bubble-busting report soon. For now however, here is one spectacular quote that finally confesses the truth about Australian banks' new role as wards of the Australian state. There is no need to hide it anymore, they own us:

External shocks are potentially more problematic. A major commodity price decline for example could see foreign investors seek to lower their exposure to Australian banks. Australia’s heavy reliance on global capital means this would be an unsettling scenario. A collapse in global liquidity following the Lehman Brothers bankruptcy in 2008 caused global investors to cut their exposures to foreign borrowers and Australian banks were among those borrowers that suffered. The Federal Government’s response included temporarily providing banks with a government guarantee on bond issuance. Markets rebalanced and the guarantees settled the anxieties of foreign lenders. However this was in the context of a global liquidity crisis where all governments of debtor nations provided such guarantees.

A similar globally coordinated response by governments could be expected in the extremely unlikely event of a second global financial crisis.

If Australia was specifically hit by a commodity-driven crisis, investor sentiment towards an individual country requiring a government guarantee for its banks might be less understanding. Nevertheless we expect that investors’ decisions would essentially be driven by their assessments of the state of the domestic economy.

No ifs, no buts. No discussion. Just the simple assumption that if the bank gets into trouble on the liability side of its balance sheet, it'll be be bailed out with a new guarantee. Stunning moral hazard in action.

Update

Well, this blogger has waded through it and just as the comments of his fellow bloggers below suggested, it is more of the same claptrap seen in the CBA and Fitch reports.

The only point of interest is that which is pulled out and highlighted above. Bill Evans' claim that his foreign-debt guzzling bank will be bailed out in the event of a terms-of-trade correction that hits housing. He offers no analysis or stress testing of the Budget in such a scenario. Yet it is obvious to this blogger that any such guarantee will be far more problematic second time around. Nor does Evans bother with any analysis of the costs of any such bailout to the Budget and the services it funds. Nor is there any analysis of the costs to the Budget after the event. Just assumptions and breathtaking arrogance.

This blog presents for your viewing pleasure, the Westpac report...

AustralilanHousing_October2010

Grantham responds

Global bubble maestro, Jeremy Grantham has responded to the deluge of criticism coming from such housing interests as CBA and Christopher Joye. Here is the money extract and full newsletter below:

I happily concede that the U.K. and Australian housing events are not your usual bubbles. Australia, though, does pass one bubble test spectacularly: we have always found that pointing out a bubble – particularly a housing bubble – is very upsetting. After all, almost everyone has a house and, not surprisingly, likes the idea that its recent doubling in value accurately reflects its doubling in service provided, e.g., it keeps the rain out better than it used to, etc. Just kidding. So, the house is the same. Perhaps the quality of the land has changed? In any case, Australians violently object to the idea that their houses, which have doubled in value in 8 years and quadrupled in 21, are in a bubble.

The U.K. and Australia are different partly because neither had a big increase in house construction. That is to say that the normal capitalist response of supply to higher prices failed. Such failure usually represents some form of government intervention. In Australia, for example, the national government sets the immigration policy, which has encouraged boatloads of immigration, while the local governments refuse to encourage offsetting home construction. There has also been an unprecedentedly long period of economic boom in Australia, and the terms of trade have moved in its favor. And, let’s not forget the $22,000 subsidy for new buyers. But does anyone think that bubbles occur without a cause? They always need two catalysts: a near-perfect economic situation and accommodating monetary conditions. The problem is that we live in a mean-reverting world where all of these things eventually change. The key question to ask is: Can a new cohort of young buyers afford to buy starter houses in your city at normal mortgage rates and normal down payment conditions? If not, the game is over and we are just waiting for the ref to blow the whistle. In Australia’s case, the timing and speed of the decline is very uncertain, but the outcome is inevitable. For example, the average buyer in Sydney has to pay at least 7.5 times income for the average house, and estimates range as high as 9 times.

With current mortgage rates at 7.5%, this means that the average buyer would have to chew up 56% of total income (7.5 x 7.5), and the new buyer even more. Good luck to them! In the U.K., which also has fl oating rate mortgages and, in this case, artifi cially low ones, the crunch for new buyers will come when mortgage rates rise to normal. But even now, with desperately low rates, the percentage of new buyers is down. Several of these factors, which do not apply to equities, make for aberrant bubbles, and clearly the Australian and U.K. housing markets fit the bill. In comparison, the U.S. and Irish housing bubbles behaved themselves. So let’s see what happens and not get too excited. After all, these may be the fi rst of 34 bubbles not to break back to long-term trend. There may be paradigm shifts. Oil looks like one, but oil is a depleting resource. If we could just start depleting Australian land, all might work out well.

JGLetter_NightofLivingFed_3Q10

Corporate dissonance

According to Elisabeth Knight at the SMH:

If BHP's management is to be criticised for this offer it should be on the basis of potentially under- estimating the political backlash from the Canadians. It is too early to make that call, given the final adjudication has not yet been made. BHP knows from recent experience how the best-laid business plans can be scuttled by governments and regulators.

Fair enough, this blogger supposes.

But then again, the deal looks pretty shot. Not least because of the ominous silence emanating from Matthew Stevens at The Australian who chooses to write on NAB today. Given his spectacular sources at BHP, (as Crikey revealed, Stevens is married to "BHP Billiton media relations chief Sam Evans") if there was a positive story to tell, he would have it.

So assuming the deal is stuffed, the question has to be asked, why has BHP learned nothing form its two previous failures with regulators?

Indeed, this is a broader question that should also be asked of corporate Australia.

Why, for instance, is the ASX pursuing a sellout strategy (if it can be called that) to SGX, which also looks seriously doomed at the regulatory level. Why, first, did they not see this backlash coming? And second, why did they not pursue a JV? (There is the possibility that the takeover is a straw man designed to get a JV approved, but that seems a stretch).

This blogger puts it down to a globalising of Australian corporate culture. Australian corporates have been operating in a competition-free environment for so long that they no longer consider, or even have the skill set for, the regular day-to-day operations of green-fields commerce.

They are specialists at asset-trading. Not really businesspeople at all. Certainly not entrepreneurs. More like corporate bureaucrats trading footy cars with their mates. For years they have faced little or no regulatory opposition to the point now where regulatory acquiesence is assumed.

And now they're taking it global, either buying or selling and running into a little trouble. It is tempting to see the failed Macquarie model as the ultimate expression of this phenomenon.

When the resources boom dies, we'll need to be looking elsewhere than corporate Australia for new industry formation.

...Sell the fact

If you value your sanity, don't listen to the day-to-day drivel of market prices. Markets are down because the WSJ has published a story, rumoured to be leaked form the Fed, describing the new QE program. Here's the money quote:

Unlike in March 2009, when the Fed laid out a program to buy $1.75 trillion worth of Treasury and mortgage bonds over six to nine months, officials this time want flexibility as they assess if the program is working.

Mr. Bernanke has used the analogy of a golfer with a new putter: Unsure how it will work, he finds best strategy is to tap lightly at first and keep tapping until the golfer figures out how best to use the putter.

The Fed could leave open the possibility of more purchases in the future, particularly if inflation is projected to remain below 2% and the unemployment outlook remains high, which is currently the expectation of many officials. Or it could halt the program if the economy or inflation surprisingly take off, officials have said.

...The main aim of a bond buying program would be to drive down long-term interest rates by pushing up the price of Treasury bonds and thus driving down their yields. From nearly 4% in April, the yield on the 10-year Treasury note has already tumbled to about 2.6%, in part because investors expect the Fed to be in the market buying bonds. Mortgage rates, closely tied to the 10-year note yield, have fallen to their lowest levels in more than four decades.

...A Wall Street Journal survey of private sector economists in early October found that the Fed is expected to purchase about $250 billion of Treasury bonds per quarter and continue until mid-2011, amounting to about $750 billion in all.

New York Fed president William Dudley put forward one key benchmark in a speech earlier this month. He noted that $500 billion worth of purchases had the same impact on the economy as a reduction of the federal funds rate by one-half to three-quarters of a percentage point.

In speeches this week, Mr. Dudley repeated he found the economy's weak state "unacceptable" and said "further Fed action was likely to be warranted."

The bond-buying program is likely to focus on Treasury bonds with maturities mostly between 2-years and 10-years, according to interviews with some officials."

One of this blogger's favourite Fed watchers, Tim Duy, goes a bit nuts over this today, describing it thus:

Federal Reserve policymakers must be pleased with themselves. Market participants have fallen in line like lemmings off a cliff pursuing the obvious trades as the excitement over quantitative easing builds. Equities, bonds, commodities are all up. Dollar is down. Perhaps more importantly, measured inflation expectations have trended higher. Psychology is a powerful thing. Like leverage.

But like leverage, psychology can turn against you. The psychology of market participants forms on the back of expectations, which in this case is for the Fed to announce a significant expansion of the balance sheet on November 3. If the Wall Street Journal is correct, the Fed is poised to disappoint those expectations with an announcement of "a few billion dollars over several months." This looks like a clear effort to temper expectations.

How can Federal Reserve Chairman Ben Bernanke not view this as anything but yet another major policy error? The first supposedly "shock and awe" balance sheet expansion failed to reflate the economy. What kind of expectations should we have for the "shock and disappoint" strategy? And the stakes are even greater. Market participants already dutifully followed the first reflation attempt, and have eagerly embraced the second. Just exactly how many bites at the apple does Bernanke expect he is going to get? Fool me once….

Whilst this blogger is well aware of the possibility of policy irrationality, this criticism looks a bit rich. If we go back to Bernanke's Jackson Hole speech, which sparked the huge rally in risk assets, what is being delivered looks pretty much on cue with what was foreshadowed:

This morning I have reviewed the outlook, the Federal Reserve’s response, and its policy options for the future should the recovery falter or inflation decline further.

In sum, the pace of recovery in output and employment has slowed somewhat in recent months, in part because of slower-than-expected growth in consumer spending, as well as continued weakness in residential and nonresidential construction. Despite this recent slowing, however, it is reasonable to expect some pickup in growth in 2011 and in subsequent years. Broad financial conditions, including monetary policy, are supportive of growth, and banks appear to have become somewhat more willing to lend.

Importantly, households may have made more progress than we had earlier thought in repairing their balance sheets, allowing them more flexibility to increase their spending as conditions improve. And as the expansion strengthens, firms should become more willing to hire. Inflation should remain subdued for some time, with low risks of either a significant increase or decrease from current levels.

Although what I have just described is, I believe, the most plausible outcome, macroeconomic projections are inherently uncertain, and the economy remains vulnerable to unexpected developments. The Federal Reserve is already supporting the

economic recovery by maintaining an extraordinarily accommodative monetary policy, using multiple tools. Should further action prove necessary, policy options are available to provide additional stimulus. Any deployment of these options requires a careful comparison of benefit and cost. However, the Committee will certainly use its tools as needed to maintain price stability - avoiding excessive inflation or further disinflation - and to promote the continuation of the economic recovery.

As I said at the beginning, we have come a long way, but there is still some way to travel. Together with other economic policymakers and the private sector, the Federal Reserve remains committed to playing its part to help the U.S. economy return to sustained, noninflationary growth.

No, on this occasion it's not Bernanke that screwed up, it's regular market hysterics. Buy the rumour, sell the fact, don't you know.

bernanke20100827a

Thursday October 28: Buy the rumour...

The QEII plan. WSJ

Bernanke's backflip. QEII little. Tim Duy

Buy the rumour, sell the fact. Bloomberg

Orwell's curse: G20 resumes currency war. Bloomberg

FT disagrees. FT

Naked Capitalism disagrees with FT. Naked Capitalism

Wall St's new gambling model. Michael Lewis

Mortgage insurance bailout. Chris Whalen

Greece sick! Bloomberg

Why does The OZ persist with Frank Gelber?

Nick Xenophon approves senate bank enquiry. BS

Are commodities in a bubble? Seeking Alpha

Food gets Dutch Disease. BS (h/t The Lorax)

Bernanke's backflip. QEII little. Tim Duy

Buy the rumour, sell the fact. Bloomberg

Orwell's curse: G20 resumes currency war. Bloomberg

FT disagrees. FT

Naked Capitalism disagrees with FT. Naked Capitalism

Wall St's new gambling model. Michael Lewis

Mortgage insurance bailout. Chris Whalen

Greece sick! Bloomberg

Why does The OZ persist with Frank Gelber?

Nick Xenophon approves senate bank enquiry. BS

Are commodities in a bubble? Seeking Alpha

Food gets Dutch Disease. BS (h/t The Lorax)

Wednesday, October 27, 2010

Slow Australia (not for the faint of heart)

Today's links have a range of pieces discussing China's development model and its possible slowdown. In the Reuters' piece, a range of analysts describe the middle-income trap awaiting China. That is the historical phenomenon of developing economy growth stagnating once average incomes hit the $7000 range. Here's the money quote from the piece:

According to data compiled by the late economic historian Angus Maddison and cited by Morgan Stanley, about 40 economies have attained a per capita GDP level of $7,000 over the past century or so.

Remarkably, the average growth rate of 31 of those 40 countries was 2.8 percentage points less in the decade after the $7,000 inflection point was reached than in the preceding decade.

Japan and South Korea hit the $7,000 mark around 1969 and 1988, whereupon their annual average GDP growth rates decelerated in the following decade by 4.1 and 2.4 percentage points respectively, Morgan Stanley calculates.

China's per capita GDP today is less than $4,000 at market exchange rates, but the bank reckons it reached Maddison's magic number, which is based on purchasing power, in 2008.

"If history is a guide and the law of gravity applies to China, China's economic growth is set to slow," Morgan Stanley said in a recent report.

China's slowdown might be gentler given its continental-sized economy and the potential for catch-up in the poorer interior. But the development experience of its neighbors, including Taiwan, is a benchmark too powerful to ignore.

Morgan Stanley has penciled in average GDP growth of 8.0 percent a year from 2010-2020, down from 10.3 percent from 2000-2009.

Slower, though, can mean a better balance. In Japan and South Korea consumption and labor income rose sharply as a share of GDP in the decade after growth peaked, while their service sectors expanded strongly.

There is a double blow here for Australia. Not only is it a slower China, but its growth mix is less favourable to the key commodities of iron ore and metallurgic coal as it moves away from fixed investment and towards consumption.

This blogger agrees this is a likely outcome for three reasons. First, China is experiencing a shift to higher labour costs. Second, external pressures arising from the trade imbalance with the US give it no choice but to rebalance internally. And third, this blogger sees no evidence that China will be able to make the political shift to greater freedoms needed if it is to further liberalise its economy and escape the trap like Korea has been able to. As a continental economy, however, China should fare better than Japan because of its greater growth sources.

Now, the course of development never did run smooth, and this blogger does not expect this change in Chinese growth to happen overnight. Indeed, as Michael Pettis argues when comparing internal rebalancings for Japan and China today:

It seems to me that the longer the Japanese distortions (especially repressed interest rates) were in place, the more debt built up, the more the large and growing capital-intensive sector required cheap capital to survive, and the harder it was to adjust interest rates. China seems to me very reliant on the same set of polices, especially very cheap capital, and it may be just as hard for them to adjust. For those who haven’t read my earlier pieces and wonder what cheap capital has to do with domestic imbalances, remember that cheap capital transfers income from net savers (households) and so reduces household consumption. It is, in my opinion, the single most important cause of China’s low consumption.

To get back to Japan’s experience, remember also that when the yen was finally forced to revalue after 1985, as the renminbi will almost certainly be, Tokyo responded to the potential slowdown with the only tool it had – investment expansion and lower real rates. This is also the only tool Beijing has, and it will almost certainly use it, making the current account adjustment even worse.

In that event, then, China's slowdown is actually likely to be preceded by a blowoff period in its fixed-investment. Even though Chinese authorities are well aware that this is a danger.

So, we have two possible scenarios for a slowing China. The first is a slow stagnation as rising costs and exchange rates crimp competitiveness or a response to that of ramping up credit and blowing off.

This blogger has no idea which of these is going to happen. And to a degree it doesn't matter.

The bottom line is that it will, most likely, happen. Where does that leave Australia?

The first point we need to understand is that commodity markets are now operating like asset markets, as discussed in this post. That is, they're driven as much by liquidity and behaviour as they are the fundamentals of supply and demand.

Such markets do not rise and fall gently. They form bubbles, such as we have now in some metal prices, and then suddenly, some shock sends them through the floor. So, for a start, commodity prices are unlikely to signal changes in China by falling in advance of, or in the early stages of, any slowdown. They will more likely follow it all at once.

Afterwards, as the growth of the China bid diminishes or reaches a plateau in global commodity markets, then the knock-on effects for commodity prices will be very large. The below chart shows how the China bid has raised the price of Australian resource exports to all destinations. When China slows they will all fall.

When that happens this blogger expects the chart below to matter a great deal. Australian productivity growth is at its lowest in the history of the chart. Moreover, the currency is at record highs and the real exchange rate (including inflation) is higher still. In short, Australian competitiveness is galloping backwards.

Even more disturbingly, these chickens are coming home to roost first in our non-resource tradable sectors, meaning our external position is even more dependent upon resource exports.

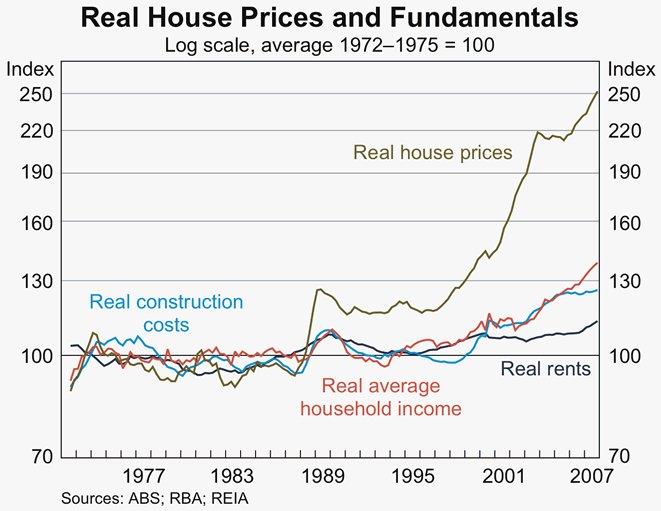

Why has this not mattered so far? It's pretty simple. Take a look at two lines on the below chart. The first and most obvious to note is house prices. Second, and just as importantly, is the rocketing red line "real average household income".

Australia's lack of competitiveness has been masked by wealth effects in housing and the extraordinary income flood from high commodity prices expressed through low unemployment, rising wages, high equity prices and lower taxes.

So, what happens when the commodity prices fall? If we're lucky, it will only be the slow reverse of these five factors as we get poorer.

If we're unlucky, and it happens all at once, this blogger's great fear, the world will run out of patience quickly and reprice our debt. Then the following chart is all that will matter:

BTW, this is behind the times. The blue line is now through the top of the chart.

BHP digs us a hole

Don't say this blog didn't warn you.

From the SMH today, BHP's Potash bid is in deep trouble:

Saskatchewan's premier said Australia wouldn't approve of BHP Billiton's foreign takeover of Potash Corp and Canada shouldn't either.

Premier Brad Wall continued to step up the pressure to make sure Canada's federal government blocks what would be the world's largest takeover this year.

Wall noted that Australia considers whether a proposed investment may result in an investor gaining control over market pricing and production, and said a particular concern to them is the extent to which it would allow an investor to control the global supply of a product.

Wall said it just isn't in the strategic interest of Canada to allow a foreign takeover of a company that controls more than 25 per cent of the world's reserves of potash.

"Given the size of this deal Australia would say no," Wall said in an interview with The Associated Press.

Wall said Australia's foreign investment review process spells out some of the very same concerns they have been using to assess BHP's bid.

These are precisely the problematic terms that this blogger outlined a couple of weeks ago. And it gets worse:

Opposition Liberal leader Michael Ignatieff urged the government to reject the deal in Parliament on Tuesday and noted four former leaders of Saskatchewan are against the deal. Government House leader John Baird responded by saying they would block the deal if it's not a net benefit to Canada.

Two Saskatchewan ministers, including Energy and Resources Minister Bill Boyd, met with the federal government on Monday. Wall said the federal government is looking very carefully at the deal and at the position of the provincial government.

...But Wall reiterated on Tuesday that his stance is not a bargaining position and that BHP can't overcome his concerns about a foreign company controlling more than 25 per cent of the world's supply of potash in Canada.

Looks like the local governor is going to take the heat off the national government in rejecting the bid.

You can hardly blame Canada for having misgivings. BHP has proved itself incapable of responsible behaviour in monopoly markets. For those interested in some history around this try The Diplomat.

If the bid is rejected, then it marks two turning points so far as this blogger is concerned. First, this will be Marius Kloppers' third attempted monopoly play in as many years. It's becoming an expensive habit (roughly a billion dollars wasted). He should either get back to running a business instead of a vested interest or give someone else a go.

Second, the big miners' greed is now doing the Australian national interest explicit harm. Getting into alternative commodities like potash makes a lot of sense long term but if the miners are going to be rebuffed because of their history of gouging then Australia is going to face a devil of a time weaning itself from its iron ore and coal dependency. We're being boxed in.

Links October 27: Slow China

China to slow to 8% growth forever. Reuters

Same topic but less convincing. Zero Hedge

One man, one vote in China. Gideon Rachman

China versus Japan vis. internal rebalancing. Michael Pettis

Mervyn King: break up the banks. Telegraph

And some distance to the rear, Peter Martin says Hockey is right.

Chewing on his dust, Jessica Irvine sort of agrees.

American house price plunge. Calculated Risk

And one less dire indicator. Calculated Risk

Arcellor predicts ongoing weak steel demand. Reuters

New five year plan for China's steel. Steel Orbis

Same topic but less convincing. Zero Hedge

One man, one vote in China. Gideon Rachman

China versus Japan vis. internal rebalancing. Michael Pettis

Mervyn King: break up the banks. Telegraph

And some distance to the rear, Peter Martin says Hockey is right.

Chewing on his dust, Jessica Irvine sort of agrees.

American house price plunge. Calculated Risk

And one less dire indicator. Calculated Risk

Arcellor predicts ongoing weak steel demand. Reuters

New five year plan for China's steel. Steel Orbis

Tuesday, October 26, 2010

Last redoubt of the cowboy capitalists

Der Spiegel published a brilliant study of the current pricing dynamics in the copper market this week. It is a fascinating and terrifying glimpse of the evolution of global capital's shiny new bubble: metals. From the piece:

In Manhattan, only one block from Ground Zero, 12 men are sitting at a round table in a windowless room. If it weren't for the countless flashing screens and electronic display panels, they might resemble a group of old men who had gathered to play poker. But these men are copper traders who have gathered at the New York Mercantile Exchange (NYMEX), the world's largest physical commodity futures exchange.

They trade in futures contracts, or agreements that obligate them to sell highly pure copper at a fixed price on a specific date. Each contract represents about 11 tons, with a current market value of roughly $95,000.

Sometimes they go "long," which means betting that prices will rise. Or they take short positions when they expect prices to fall. These traders no longer have any interest whatsoever in the metal itself.

Traders today deal in unimaginable sums worldwide, with securities worth more than $20 billion changing hands every day. Last year, copper futures corresponding to 1.13 billion tons were traded on the world's four largest copper exchanges, in London, New York, Shanghai and Mumbai. It was 71 times as much copper as the industry actually produced in the same period.

For any Australian wishing to understand the world into which we are being swept like a bobbing cork, this is a must read. As the above chart from the article illustrates, copper, like oil before it, is trading on an incredible balloon of virtual demand. The article continues:

Price movements are no longer as dependent on the so-called fundamentals. Nowadays, commodities prices are largely a question of emotion. Of course, this doesn't mean that supply and demand no longer play a role for speculators. On the contrary, speculators eagerly follow every piece of news on residential construction in China, ore production in Chile or inventories in London. The problem is that the market only takes notice of news that reflects its mood. Everything else is glossed over. This can lead to grotesque overreactions and extremely volatile prices, to the detriment of consumers and the economy.

Peter Hollands, a British geologist, recognized early on that a deep-seated change was taking place. Hollands, an authority in the copper business, owns a consulting company called Bloomsbury Minerals Economics, tucked away on a side street near London's West End. "We have been living in a new world for the last six years," says Hollands.

Six years ago, a "wave of liquidity" took hold of the market and moved prices in an unprecedented manner, says Hollands. He points to a chart showing two different copper prices (see graphic). One of the lines on the graph is notional. It rises only moderately after 2004 and doesn't exceed $5,000 per ton. It is the result of the traditional factors that influence the price of copper, such as production costs, inventory levels, industrial orders and the effects of currency movements. This line describes the old world, "when copper was still a simple industrial metal," Hollands says, a touch of melancholy in his voice.

The other line shows the actual changes in the price of copper, how it shot up to over $8,000 and has been hopping nervously up and down since then. This is the new world, the world of finance-driven commodities markets. They are no longer shaped by the market and its forces, but by what the market believes -- or what it is supposed to believe.

This is the real world of markets that confronts our policy-makers. And, as discussed in previous posts, it applies just as readily to the pricing of commodity currencies as it does to the underlying goods.

According to Ilene Grabel and Ha-Joon Chang writing in the FT, there is widespread and growing acknowledgement amongst global policy-makers of the damage these maniacal markets do:

Was it really just over a decade ago that the International Monetary Fund and investors howled when Malaysia imposed capital controls in response to the Asian financial crisis? We ask because suddenly those times seem so distant. Today, the IMF is not just sitting on its hands as country after country resurrects capital controls, but is actually going so far as to promote their use. What about the investors whose freedoms are eclipsed by the new controls? Well, their enthusiasm for foreign lending and investing has not been damped in the least. So what is going on here? In our view, nothing short of the most significant transformation in global financial management of the past 30 years.

Like most transformations, this reform has been gradual. Reform in the IMF view of capital controls actually began soon after the Asian crisis, as countries such as Chile, China and India imposed controls. Most analysts found that these controls were beneficial in key respects. This success led the IMF to soften its hardline stance: it admitted that controls might be tolerable in exceptional cases provided that they were temporary, market friendly and focused strictly on capital inflows. That said, policymakers adopted capital controls at their peril – not least risking condemnation by the Fund and by credit rating agencies, and punishment by international investors.

What was just a trickle of controls before the current crisis is now a flood. Iceland led the way in 2008 as it grappled with its financial implosion. Soon after, a parade of developing countries took action: some strengthened existing controls while others introduced new measures that targeted inflows and outflows. For example, during the crisis China augmented its extensive array of controls, while Indonesia, Taiwan, Peru, Argentina, Ecuador, Ukraine, Russia and Venezuela also introduced controls of one sort or another. In October 2010 alone: Brazil twice raised its tax on foreign investment in fixed-income bonds while leaving foreign direct investment untaxed; Thailand introduced a 15 per cent withholding tax on capital gains and interest payments on foreign holdings of government and state-owned company bonds; and South Korean regulators have begun to audit lenders utilising foreign currency derivatives.

This blog just can't understand why Australia is not having this discussion. Like copper, the Aussie dollar is grossly inflated. Moreover, the real exchange rate, which includes inflation, has been rising even more for years.

Fact is, we've got ourselves into a major pickle. If we undertake currency control initiatives it would mean interest rates would have to be higher to control the boom. That means more pressure on housing just when its entering a correction.

And we've trashed a resource rent tax as an alternative.

So instead, we're gonna sacrifice our non-resource exports to houses and holes.

Inexplicably to this blogger, Chris Richardson joined the unholy consensus today when he uged:

The government to refrain from erecting new trade barriers, subsidising old industries and reaching for regulation without checking if its costs outweighed benefits. And don't chase the chimera of 'supporting jobs' in an economy that is already close to full employment.

Whilst in virtually the same breath agreeing with this bloggers' forecast outcome:

Mining and construction were the main industries set to ''turbocharge'' the economy in years ahead. It said the mining industry's growth rate would top more than 7 per cent this financial year and next, while a recovery in new home building would lift construction's output by as much as 9 per cent this year.

And after that?

No Joe (updated)

Here's a scorecard for Joe Hockey's nine point plan on bank re-regulation. This blogger can see why the Australian Bankers Association responded positively. Not much to fear here.

1. Let’s give the ACCC power to investigate collusive price signalling (that is, oligopolistic behaviour), which is exactly what Graeme Samuel has called for.

H&H: And what's he going to do when he points to the obvious?

2. Let’s encourage APRA to investigate whether the major banks are taking on unnecessary risks in the name of trying to maximise short-term returns that conflict with the preferences of those that backstop the system, namely taxpayers;

H&H: They already do this. They've stress tested. They're preparing liquidity requirements. Hockey needs to put out some terms of reference around this or it's going nowhere.

3. Let’s formally mandate the RBA to publish regular—rather than irregular—reporting on bank net interest margins, returns on equity, and profitability so that we can all determine whether the major banks are extracting monopolistic profits; that is, whether taxpayers are effectively subsidising supernormal returns;

H&H: Ummm...these are published every month already

4. Let’s investigate David Murray’s proposal for Aussie Post to make its 3,800 branches available as distribution channels for smaller lenders. To be clear, the Coalition does not endorse Australia Post assuming balance-sheet risk and getting into the banking business itself;

H&H: So why investigate it then?

5. Let’s ask the Treasury and the RBA to investigate ways to further improve the liquidity of the residential and commercial mortgage backed securities markets, which are an alternate source of funding for smaller lenders, including consideration of the Coalition proposal to extend the Government’s credit rating to AAA rated commercial paper in those markets to improve liquidity;

H&H: NO! Let's not. Securitisation is part of the problem, not the answer to it.

6. Let’s explore further simplification of my beloved Financial Services Reform Act, to make the business of actually getting out and doing business easier and simpler;

H&H: Admirable I suppose but not terribly relevant.

7. Let’s direct APRA to explore whether the risk-weightings on business loans secured by residential properties are punitive. Many small businesses tell me that they do not receive sufficient financial benefit from pledging their family home to secure their borrowings;

H&H: Great idea. It's a grossly under-appreciated fact that much Australian small business is underpinned by homes.

8. Let’s commission a resolution to the debate about whether the banks should be able to issue “covered bonds”, in the same way other jurisdictions allow their banks to, which provides a more affordable line of credit;

H&H: Well...maybe...but although such bonds are rock solid for investors they can make it harder for banks under pressure because no bond haircuts are possible.

9. And let’s wrap up all of this work into a full review of the financial system—a Son of Wallis, or Grandaughter of Campbell, whatever you will.

H&H: Bring it on but not on these terms of reference.

With equal measures of hope and despair, and for the purposes of debate, here is Houses and Holes own nine point plan:

1. Let's mandate that APRA and the RBA publish regular and detailed statistics on both repo operations and offshore borrowing profiles for individual banks.

2. Let's mandate that the banks will never again receive a wholesale funding bailout.

3. Let's explore an FDIC-like institution that guarantees offshore borrowing through insurance premiums paid by the banks into a collective fund. It could be set up as a counter-cyclical, macro-prudential tool sitting between APRA and the RBA with the singular goal of keeping offshore borrowing within conservative risk limits. Or, it could be used to deliberately wind down the borrowing on a sustainable timeline. This idea might alternatively be structured as a Tobin tax.

4. Or, increase capital adequacy to 20%.

5. Let's start a new government bank with a charter of competing with banks without destroying them.

6. Let's phase out negative gearing and capital gains tax breaks for property.

7. Or, abolish taxes on deposits.

8. Let's place legislative limits on bank remuneration, including a blanket ban on bonus payments.

9. Let's have a fair dinkum son of Wallis Inquiry with a credible outsider in charge.

And finally, here are some answers to the questions that I know the libertarians amongst you, dear readers, will want to yell:

No, this blogger is not a communist. Yes, it is a liberal. No, it does not want to regulate other sectors of the economy.

Update

Banking Day says:

In contrast to last week’s widely criticised media comments from the shadow treasurer, yesterday’s precisely structured speech reflected consultation with industry experts. In particular, it adopted many ideas previously advocated by Christopher Joye, influential commentator and head of financial advisory group Rismark International.

...The industry is desperate to avoid being forced into what is sometimes called the “narrow banking” model, regulated like a gas or water company and forced into accepting a low rate of return in exchange for a quasi-monopolistic position. Hockey’s remarks push the debate in this direction.

Although the nine points are very vague, to this blogger they appear to aim to take a chunk of the moral hazard currently enjoyed by the majors and hand it instead to securitisers. Hardly a new social compact.

The phrase missing from this entire discourse is "systemic risk". You aren't dealing with the huge liquidity risk in Australia's financial sector-mediated offshore borrowing just by shifting the moral hazard around.

Links October 26: Commerce not capital

Joe's nine point plan to nowhere. Joe Hockey

What copper can tell us about the dollar. Der Speigel

Why capital controls rock. FT

NYC as a microcosm of ForeclsoureGate. Naked Capitalism

Bill Black as a macrocosm of ForeclosureGate. MSNBC

Too small the stimulus. Paul Krugman

US housing inventory. Calculated Risk

Resentments between the rising and falling. FT

Soft bids for ore. Reuters

What copper can tell us about the dollar. Der Speigel

Why capital controls rock. FT

NYC as a microcosm of ForeclsoureGate. Naked Capitalism

Bill Black as a macrocosm of ForeclosureGate. MSNBC

Too small the stimulus. Paul Krugman

US housing inventory. Calculated Risk

Resentments between the rising and falling. FT

Soft bids for ore. Reuters

Monday, October 25, 2010

Not Macfarlane

The more things change the more they stay the same. From the SMH:

The shadow treasurer, Joe Hockey, will call for an inquiry into the banking system today with the National Australia Bank, Westpac and the ANZ all expected to reveal record profits.

In an address to the Australian Industry Group entitled ''It's time to talk banking'', Mr Hockey will argue that 13 years after the landmark Wallis inquiry into the financial system Australia's banks are beyond effective control and are engaging in behaviour that will put the nation at risk.

While the big four are telling investors they want to be ''growth stocks'' expanding overseas, Mr Hockey will argue Australia's interests would be better served by them ''sticking to their knitting'' as they did before the financial crisis.

... Mr Hockey will take up a call made by six prominent economists last year for a public inquiry into the financial system to be led by a respected figure such as the former governor of the Reserve Bank, Ian Macfarlane.

Bring it on. But not with Ian Macfarlane at its head. First, although Macfarlane has the reputation of a bubble buster arising from his actions in 2003, he spent the prior six plus years stoking raging house price growth, as this blogger has traced in a previous post. The shaded area in the above graph is his tenure at the head of the RBA.

Second, he also oversaw the growth of Australia's gigantic offshore borrowing in the banks and securitisers. At a Lowy Institute event last year, Macfarlane defended the banks to the hilt on these borrowings. You can listen to it here (money quotes at 35 minutes).

MacFarlane can identify the flaws in Australia's financial architecture only if he attacks his own legacy.

h/t Delusional Economics for original chart.

American housing resumes its crash

Those who believe that the danger of a double-dip recession has passed should take pause today to register an American housing market plunging with renewed vigor. As Calculated Risk reported over the weekend:

Clear Capital™ Reports Sudden and Dramatic Drop in U.S. Home Prices

“Clear Capital’s latest data through October 22 shows even more pronounced price declines than our most recent HDI market report released two weeks ago,” said Dr. Alex Villacorta, senior statistician, Clear Capital. “At the national level, home prices are clearly experiencing a dramatic drop from the tax credit-induced highs, effectively wiping out all of the gains obtained during the flurry of activity just preceding the tax credit expiration.”

This special Clear Capital Home Data Index (HDI) alert shows that national home prices have declined 5.9% in just two months and are now at the same level as in mid April 2010, two weeks prior to the expiration of the recent federal homebuyer tax credit. This significant drop in prices, in advance of the typical winter housing market slowdowns, paints an ominous picture that will likely show up in other home data indices in the coming months.

... if previous correlations between the Clear Capital and S&P/Case-Shiller indices continue as expected, the next two months will show a similar downward trend in S&P/Case Shiller numbers.

And here's Clear Capital's original release.

This was foreseen by many analysts including yours truly because of the removal of government subsidies and an ongoing huge inventory overhang. In that sense this is not unexpected and American authorities have already positioned its banks to absorb further losses by giving the investment banks access to the Fed discount window, as well as engineering a steep yield curve for easy earnings.

There are, however, two surprises here. One is the swiftness of the slide. These losses are faster than anything experienced during the first round crash.

The second is the effect ForeclosureGate will have on this trend. The FT has a very important article in this regard:

A particular worry is whether the tales of shoddy documentation completed by so-called “robo-signers” at mortgage lenders and growing foreclosure delays will affect people’s behaviour. It could for three reasons.

First, a longer gap between stopping payments and being evicted from the property allows people to build up a nest-egg. In many states, homeowners do not owe the bank anything more than the keys to their home if they default on a mortgage.

Second, a slowdown in foreclosures creates an ever-growing backlog of unsold homes, which will at some point be sold, pushing house prices lower. If people think home prices will not recover, they are more likely to throw in the towel.

Third, it further damages the reputation of the banks who made the mortgages, and this could make borrowers more unwilling to pay. “More bad news and uncertainty creates more anger against the banks and frustration with the system,” says Chris Mayer, Professor at Columbia Business School. “That’s not helpful.”

... Jon Maddux, who runs YouWalkAway.com, which advises people on the foreclosure process, says calls about foreclosures have increased recently. “The banks are cutting corners in the foreclosure process and in some cases breaking the law and that sends the message to homeowners that, if the banks are not honouring their promises, why should the homeowners?” he says.

In short, the Wall St banks' rape of the social contract has given Americans the moral cover to walk away from their mortgages.

As prices begin to fall again, there is the real prospect of a new negative feedback loop forming. In the below video, Gary Shilling predicts this toxic mix will push down housing values another 20%, almost as much as they've fallen already. He also predicts this will nearly double the number of impaired loans.

The banks may be set up to absorb losses but this is beyond the pale. It will require massive new capital raisings and kill equity prices. Not to mention MBS coming under pressure from both falling values on one hand and litigation on the other.

You can rely on the Fed to continue its quantitive easing ad infintum.

Services won't save us

Two pieces today give you the bitter flavour of what is ahead for Australian exports.

The first is a spot-on diatribe by Martin Feil at The Age.

ACCORDING to many pundits and politicians, expanding the Australian services sector is the correct (if not the only) long-term strategic direction for the Australian economy. We have completely given up on manufacturing. Agriculture is a useful source of income but doesn't create many jobs by adding value to primary production. Finally, mining is booming but all mining booms end. Sooner or later we will have nothing left.

Treasury secretary Ken Henry nominated the services sector as our strategic way forward. Estimates of employment are that more than 80 per cent of Australian workers are employed in this sector. About 73 per cent of Australian gross domestic product is derived from the sector.

This view contradicts global history and the present experience of virtually every developed country. It is simply an excuse for the poverty and hubris of our national planning and the dominance of public servants, consultancies and academics in our thinking about the future development of our nation.

Anthony Byrne is the member for Holt and was parliamentary secretary to both the prime minister and the trade minister in the first Gillard ministry. This year he addressed the Australian Services Roundtable. His topic was the challenge posed by the globalisation of services exports.

Mr Byrne spoke about the paradox of the dominance of the services sector in the Australian economy and its sharp contrast to services' share of Australian exports (21 per cent). Only 6500 services exporters were present in the total number of 45,000 exporters. The first excuse offered by the former parliamentary secretary was that the Australian Bureau of Statistics may have got the numbers wrong. The second criticism was that a lot of our services are highly protected.

Feil then takes aim at policy:

The government's economic strategy is to commit to the Doha global trade liberalisation round, Australia's six free-trade agreements and seven further deals under negotiation, and to the Brand Australia program.

It is also committed to further micro-economic reform and a major infrastructure investment to improve the profitability of our logistics companies, which are busy at ports and on roads bringing in the merchandise that we have to have. Most container ports and container yards are clogged with empty containers awaiting repositioning overseas.

Absolutely none of this is new and most of it has already failed. Brand Australia will compete with Buy Australia, which has struggled along for years without any real government interest. I wonder how much the new campaign will cost.

The simple truth is that if we employ 80 per cent of the population in activities that contribute 21 per cent of our exports, we are going to go broke.

This blogger is a supporter of globalisation strategies and of sensible liberalisation of service sectors. For instance, Coles and Woolies have higher revenues than Macdonalds but comfort with a local duopoly is one reason they've done nothing elsewhere.

Nonetheless, Feil is right that this is no solution to Dutch Disease.

Services exports of the type described are not terrestrial industries. These are people-to-people businesses that require presence on the ground. They are therefore, a story about outward flowing foreign investment, not goods. That is, Australian businesses will need to open operations in the export target country.

This has several implications. First, it means the jobs are elsewhere. Like the US corporate model of employing Chinese to make stuff to sell everyone else, this leads to an ongoing shift toward a meta or post-modern economy. Such delivers high corporate profits for a financially literate elite but does bugger all for anyone further down the food chain.

Second, although the profits from such ventures are recycled on the capital account, they tend to be minimised by the various and many manipulations available in the transfer process. Moreover, that means lower tax revenue.

Third, Australian government support is, virtually by definition, unable to do anything to support such a process. It is politically impossible to sell export subsidies that result in outgoing investment and jobs elsewhere. The only agency that will provide support for such things is EFIC, which operates as a semi-independent corporation. It has been trying to push through legislation to help in this process for years without success.

Fourth, and this is the biggest issue, Australian business is a history of failure when it comes to offshore investment. The tale of one corporate titan, Don Argus, is indicative. Compare the Homeside debacle, in which NAB bought a rust-belt based mortgage bank which became ground zero in the GFC, with his record at BHP where he exported raw materials at a rate that would make a pillaging Mongol blush.

There was some hope in the last cycle that Macquarie Bank and the listed property and infrastructure trusts had cracked it. However, that model has collapsed spectacularly and now sports such names of business infamy as ABC Learning, Centro Properties and Babcock&Brown. For a history of that try The Diplomat.

Which brings us to our second bitter pill. With the Australian dollar stronger for longer you would expect a surge in outgoing M&A investment. Not according to Bloomberg:

Australia’s corporate chiefs are spurning overseas acquisitions as concerns about the health of the global economy overshadow the record buying power of the local currency.

Australian companies have made or announced $53.7 billion of purchases abroad this year as the currency reached parity with the U.S. dollar, according to data compiled by Bloomberg. Stripping out BHP Billiton Ltd.’s $40 billion hostile bid for Canada’s Potash Corp. of Saskatchewan Inc., the amount would be the lowest since 2003.

“Now is a great time to make an acquisition offshore, but it also happens to be a time when boards generally are quite cautious about making offshore acquisitions,” said Andrew Pridham, head of Australian investment banking at Moelis & Co. in Sydney. “The appetite is not there.”

The International Monetary Fund this month said the global recovery is fragile, predicting slower economic growth worldwide in 2011. Ralph Norris, chief executive officer of Commonwealth Bank of Australia, the nation’s biggest lender, echoed that view on Oct. 20 when he called the world’s recovery “weak and uneven” and pledged a conservative approach to risk.

The fallout from failed takeovers in past years is adding to executives’ reluctance to pursue deals, said Pridham, a former member of UBS AG’s global investment banking management committee.

Sunday, October 24, 2010

One honest man

So the G20 isn't going to engage in the currency war that's already raging. The US wants a "strong dollar" and China "market-determined exchange rates". All countries are going to consider the Geithner imbalances plan already rejected. Is it this blog or did the G20 just hit new heights of Orwellian double-speak?

Anyway, came across this speech by BOE gov, Mervyn King, which was delivered to some Midlands merchants before he got on the plane. It's a little more honest:

At the G7 meeting in October 2008, I was part of the group of ministers and central bank governors who threw away the prepared communiqué, and replaced it by a bold short statement of our determination to work together. That spirit, so strong then, has ebbed away. Current exchange rate tensions illustrate the resistance to the relative price changes that are necessary for a successful rebalancing. The need to act in the collective interest has yet to be recognised, and, unless it is, it will be only a matter of time before one or more countries resort to trade protectionism as the only domestic instrument to support a necessary rebalancing. That could, as it did in the 1930s, lead to a disastrous collapse in activity around the world. Every country would suffer ruinous consequences – including our own.

The whole thing is worth a read to remind us of how big the challenge ahead is. This blogger must ask the question again: If the logical historical outcome is that the US is going to impose trade sanctions, then shouldn't we be supporting a break in the yuan peg now?

Mervyn King

Saturday, October 23, 2010

Links Oct 25: Services will save us!

Services no answer to Dutch Disease. Martin Feil

CEOs won't invest overseas despite high dollar. Bloomberg

US house prices resume their plunge. Calculated Risk

That's before ForeclosureGate hits the market. FT

Market is about...oh...halfway down. CNBC

ForeclosureGate: Unimaginable amount of litigation. NYT

Fitch prepares downgrade for Wall St on Volcker. Zero Hedge

G20's Sino kiss: Imbalance paralysis, new IMF powers. FT, FT

Geithner's imbalances plan scheduled for tea and biscuits. FT

Week ahead for the DOW. Calculated Risk

Post bank. Danny John

CEOs won't invest overseas despite high dollar. Bloomberg

US house prices resume their plunge. Calculated Risk

That's before ForeclosureGate hits the market. FT

Market is about...oh...halfway down. CNBC

ForeclosureGate: Unimaginable amount of litigation. NYT

Fitch prepares downgrade for Wall St on Volcker. Zero Hedge

G20's Sino kiss: Imbalance paralysis, new IMF powers. FT, FT

Geithner's imbalances plan scheduled for tea and biscuits. FT

Week ahead for the DOW. Calculated Risk

Post bank. Danny John

Weekend Reading

Australian houses: highest in the known universe. The Economist

Interactive chart of global house prices. The Economist

RMBS guarantee alert: GSEs still hemorrhaging. NYT, Calculated Risk

FOMC & QEII. Calculated Risk

G20 flips bird at Geithner rebalancing plan (surprise!). Reuters

Ironic, US canned Keynes' similar plan at Bretton Woods. Monbiot

God save austerity (or, QEIII). UK debt costs collapse. FT

Australia Post bank. Michael West, Malcolm Maiden

Economic conversation must be broader. Delusional Economics

Left versus Right idiocy watch. David Uren

CISA wants new ore price system. Steel Orbis

BHP fail. SMH, FT

Interactive chart of global house prices. The Economist

RMBS guarantee alert: GSEs still hemorrhaging. NYT, Calculated Risk

FOMC & QEII. Calculated Risk

G20 flips bird at Geithner rebalancing plan (surprise!). Reuters

Ironic, US canned Keynes' similar plan at Bretton Woods. Monbiot

God save austerity (or, QEIII). UK debt costs collapse. FT

Australia Post bank. Michael West, Malcolm Maiden

Economic conversation must be broader. Delusional Economics

Left versus Right idiocy watch. David Uren

CISA wants new ore price system. Steel Orbis

BHP fail. SMH, FT

Friday, October 22, 2010

Go Joe

Yesterday, Shadow Treasurer, Joe Hockey, was torn to shreds for making the most sensible suggestion regarding Australian banks that this nation has heard since the global financial crisis.

First on ABC radio and then again in a doorstop interview, Hockey made the case that the government needs to act to rein in unilateral interest rate rises. Hockey called for "...a mature debate about the future of banking here in Australia and the challenges around the world". And although he rejected recent Greens' agitation for legislation on the matter, the Shadow Treasurer rang a clarion opening bell for that debate by welcoming their ideas.

In a parliament defined by conflict this was genuine leadership.

Hockey's argument is as fresh as it is straight forward: "I am calling for a social compact between the banks, the community and the government that focuses on delivering affordable credit to Australians and does not disadvantage unfairly people who are borrowing money to buy their home."

The keystone of Hockey's position is that in its recent statement on monetary policy, the RBA called time on the bank's expanding net interest margins. According to Hockey the banks therefore have no excuse for further unofficial rate rises.

To understand each of these two important and interdependent points we need some history.

Banks are privileged businesses like no other. Their role as mediators of savings and credit give them a virtual license to print money. Yet, this position is also central to the smooth running of every dimension of an economy. There is always therefore a balance to be struck between the banks' profit and its duty of care.

Since the 1997 Wallis Inquiry the monitoring of that duty of care has been split in two. Deposit-taking banks were governed by the Australian Prudential Regulatory Authority (APRA) and its rules that banks keep certain levels of capital in reserve in case of losses, and that they do not over-leverage.

Non-banks also mediate credit but they take savings from investors which they pass onto borrowers via market-based bonds called Residential Mortgage Backed Securities (RMBS). After Wallis, they were left unregulated because investors and the market in which they operated were deemed sophisticated and efficient enough to handle themselves. Listed firms fell under the purview of ASIC like any other company.

What happened next was that the two sides of Australian financial services went to war over customers. The battle lasted ten years and by its conclusion both halves had borrowed enormous amounts of money offshore and poured it into housing mortgages.

Then, when the GFC arrived, both sides of the regulatory structure failed.

Non-banks were found to rely heavily on cheap short-term funding from investors for the long-term loans they provided customers. As the GFC gathered pace, this short-term funding suddenly became very expensive and the interest rate spread that underpinned the non-banks business model collapsed. Most were absorbed for a pittance by the banks.

When the crisis reached fever pitch after Lehman Brothers hurtled off a cliff, the banks were found to have a similar problem. They had borrowed a huge amount of money offshore and much of it was also of the cheap, short-term variety. As global markets froze, neither APRA nor the RBA had the firepower to contain the bank's bleeding.

A government guarantee of $157 billion in offshore borrowings was needed to stave off probable insolvency for all major banks and a calamity for Australia.

So neither APRA's regulations nor the market's discipline sufficed to hold banks and non-banks within the social compact outlined by Wallis.

That brings us to Hockey's second point. Since the GFC, markets have recovered enough that they will now lend Australian banks money at reasonable rates. But those rates are generally still higher than they were pre-GFC. As well, APRA has pushed banks to refinance cheap, short term offshore borrowings to more expensive longer term loans.

The banks are not kidding that their cost of funds has gone up. As each pre-GFC offshore loan becomes due it must be refinanced at a higher rate. The rise in costs is unlikely to have plateaued because APRA is not finished restructuring international bank borrowing. It has yet to impose new international rules called Basel III.

Hockey is right, however, that the banks can pass on these higher costs only because there is no competition. There is nothing to the banks' argument that they must ipso facto pass on their higher funding costs to customers. If there were healthy competition then they would simply have to wear it in lower profits. Sadly, because all of the banks borrowed monstrously offshore there is nobody left to take advantage. This is Australia's version of too-big-to-fail.

But Australia is in a bind. Hockey's suggestion for increased competition is to extend the nation's AAA guarantee to RMBS issues. This is a ludicrous solution for a number of reasons, not the least being it relies on the same Wallis structure that has just proved unacceptably vulnerable.

Unless, of course, the guarantee is permanent. In that event, Australia will have established its own version of Fannie Mae or Freddie Mac, the government sponsored enterprises at the heart of the US mortgage meltdown. That runs the risk of breeding a whole new generation of cowboy lenders sporting the badge of the sovereign.

Besides which, a surfeit of credit has already inflated the great Australian housing bubble, the most stark real economic consequence of the failure of the Wallis structure. We don't need more mortgages, we need more business lending.

A better but more difficult road is to begin the long hard slog of raising more banks. Conservatively run banks that encourage savings and local deposits.

Some hints of how that might be done are already available. A combined AMP/Axa could be encouraged into banking services. Australia Post might begin a people's bank. Perhaps some of the smaller banks can merge. Longer term these options offer greater hope of producing a more competitive banking sector without relying on expanded moral hazards.

To answer these questions, Australia desperately needs a new 'son of Wallis' Inquiry. The first question it should ask is what kind of banking system does Australia want not today but in ten years. The current piecemeal approach will only repeat the failures of history.

Only that way can we answer Hockey's last and most important question. How does Australia deal with "...a new paradigm – I hate to use those terms, but I’m sorry, don’t groan too hard – a new framework, that’s the word – we are facing a new global banking framework. This is a whole new environment we are in."

An environment we haven't even begun to explore. Opening a window on that was Hockey's greatest contribution yesterday.

This article appeared in Crikey.

211010 - Joe Hockey Transcript Doorstop (1)

Subscribe to:

Comments (Atom)