This morning, this blogger ran across a reference to the Reserve Bank of NZ's relatively new regulations regarding the Core Liquidity Ratio (CLR).

The rules have been around for almost twelve months now (which says something in itself) but are worth revisiting today to examine how a closely related nation with the same banks (and problems) is interpreting the G20 and Basel III process.

The crucial paper was released in Dec 2009 and states:

The quantitative and qualitative requirements were put in place for most locally incorporated banks through additions to their conditions of registration in October 2009. These new conditions are that the banks meet the requirements of the policy with effect from 1 April 2010. This builds in a period of transition to allow the banks sufficient time to align their internal systems with the new requirements. Thereafter, the mismatch requirements are designed to act as a floor to banks’ existing management of short-term liquidity risk, and as such, are expected to remain at the initial calibration.

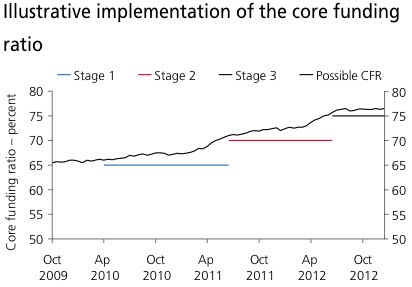

With the one-year core funding ratio, however, the Reserve Bank is seeking to lengthen banks’ maturity profiles to provide greater protection against liquidity risk in the medium-to longer term. With this in mind, the Reserve Bank intends to raise the required minimum in the future from the initial 65 percent minimum requirement. It expects to do this in two further stages, with the minimum raised to 70 percent at the second stage, and then finally increased to the expected long-term minimum of 75 percent. Most banks will need to adjust their funding profiles to meet the requirements in Stages 2 and 3.

In short, the RBNZ is forcing the Australian banks that dominate it's financial system to alter the maturity profiles in the their wholesale borrowings.

If you read the Reserve Bank Governor Alan Bollard's book, Crisis, it is not hard to see why our kiwi cousins have adopted strong measures. Basically they don't trust Australia's big banks and want to ensure New Zealand is in a position to weather another crisis, even if the parent firm's don't (which is fine in theory).

That is where the juxtaposition with Australian authorities is interesting. Rather than relying on Invisopower! to disguise the extent of Australian bank vulnerability to another liquidity shock, RBNZ has published comprehensive studies on the issue and acted decisively for both greater stability and lower moral hazard.

Moreover, the mooted changes in Australia's liquidity regime are much less onerous than those in New Zealand. The RBA's last communique on the issue serves:

The second key aspect of the reform proposals is a range of stricter global liquidity requirements to ensure that bank assets remain prudently liquid in periods of stress, and that banks' funding is on a more sustainable, longer-term basis. The liquidity proposals include requirements based on two new ratios, both of which may reduce the traditional maturity transformation role of banks.

The liquidity coverage ratio (LCR) requires banks to have sufficient high-quality liquid assets to fund projected cash outflows in a hypothetical 30-day crisis situation.

The net stable funding ratio (NSFR) requirement aims to match the duration of banks' liabilities and assets more closely by comparing liabilities considered stable (such as deposits and long-term debt) with longer-term assets (such as loans).

The liquidity proposals have been amended in several areas compared with those released in December 2009, which have the cumulative effect of making them somewhat less onerous. For example, for the LCR, assumed rates of certain deposit outflows (or ‘run-off’ rates) for retail and small business deposits held with banks were lowered, resulting in more funds assumed to remain with the bank during a stressed scenario. Also, outflows of funding by governments and central banks are assumed to be lower than previously proposed, in recognition that, with secured funding in particular, the authorities are likely to continue to roll-over their funding during a time of stress. After an observation period starting in 2011, the LCR will be introduced from 2015.

... The NSFR has been modified and its introduction delayed. The revisions largely reflect feedback that the initial calibration was too severe, as well as concerns regarding the perverse incentives it created, in particular that it would favour investment banking over retail banking. There will also be an ‘observation phase’ before implementation, to address any unintended consequences across business models or funding structures before the revised NSFR is finalised and introduced from the start of 2018.

We aren't comparing apples with apples, so it's not possible to be precise about much weaker the Australian liquidity measures are. However, this blogger has it on good authority that they are considerably weaker. It is also obvious that the Australian time frames for implementation are much more generous. The above image is indicative only but shows NZ's serious intention, and the measures are already underway.

Not only that, despite APRA's strong rhetoric, we have a parliament in uproar over anything that offers the whiff of increased bank funding costs and rate rises.

We can draw several conclusions from all of this. Like much of its strategic policy, NZ enjoys a certain moral hazard in its relations with Australia and so it can afford to strike more idealistic positions.

Or, New Zealand is doing a much better job than we are.

Either way, New Zealand's regulators hold the unique perspective of being both dependent upon our banks and being outside of our regulatory authorities. It's difficult to not also conclude that when they peer across the Tasman, they don't like what they see.

2009dec72_4hoskinneildrichardson

No comments:

Post a Comment